Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

5 Qualities to Look For in a Real Estate Agent

If you’re thinking of buying a home or selling your current one, choosing the right real estate agent can make a world of difference. While it’s easy to find many highly rated Realtors online, a great agent should meet a set of criteria. They don’t merely facilitate transactions; they serve as your trusted advocate, a local expert, a strategic project manager, and more. Here are five essential qualities to look for in a real estate agent.

Local Expertise

Your real estate agent should possess a deep understanding of the local market. Local Realtors can explain the nuances of neighborhoods, school districts, and market trends. Their insights can help you find a property that fits your needs, lifestyle, and budget. Additionally, if you’re a first-time homebuyer, buying a new construction home and/or looking for a local lender, their connections and advice will help you make more informed decisions.

For sellers, a local agent can provide a Comparative Market Analysis to properly price your home. This ensures your property attracts serious buyers quickly. From top-notch repair workers to great stagers to effective local marketing outlets, a well-connected agent in your area can be highly advantageous. Additionally, our local Windermere agents offer special programs such as the Windermere Bridge Loan, which enables you to buy before you sell. If you want to make needed repairs/updates that will give you a competitive edge in your local market, the Windermere Ready program can provide an upfront investment of up to $100,000.

Strong Communication Skills

Real estate transactions involve many tasks and professionals. So, having an excellent communicator on your team is essential. Look for an agent who is known for being a good listener and keeps clients informed throughout the process. You also want someone who answers questions promptly and effectively negotiates on your behalf. A local agent often has strong relationships in the community, including with local lenders, other Realtors, and inspectors. This can streamline the entire process and make communication more efficient.

Proven Track Record

An agent with an established reputation in your local area will have the credibility to back up their claims. Look at their sales portfolio and their client testimonials. While online reviews don’t tell the whole story, they can certainly give you a sense of whether an agent would be a good fit. When looking at their past transactions, reviews, and designations, you may want to scan for specific areas of expertise that would benefit you. For example, have they bought or sold waterfront properties? Do they have any certifications or specialties relating to retirees, investors, or military clients? A local agent’s familiarity with the market, different situations, and/or particular properties demonstrates how that agent’s proven track record could specifically benefit you.

Attention to Detail

Having an agent who pays close attention to the details can prevent costly mistakes. From touring homes to conducting inspections, a keen eye matters. It also impacts negotiations and contracts. A detail-oriented agent is an incredible asset. Your knowledgeable guide should also be able to explain regional regulations and potential issues, showing their mastery of those particulars. Also, they are there to help you manage all of the details involved in a transaction. Their meticulousness should help you achieve the best possible outcome.

A Dedicated Real Estate Agent

Homes on the market can pop up or vanish quickly. You need a real estate agent who is committed to your goals as a homebuyer or seller. While they’ll probably have other clients to juggle, you want someone who is ready to assist you and can make your needs a top priority. Local agents often have more availability because they aren’t traveling long distances to tour homes or to help you prepare your own for the market. They also tend to be more available to meet and handle last-minute issues or inquiries.

Windermere’s slogan is “All in, for you”, and our agents exemplify that. Whether you choose a Windermere agent or not, we hope you’ll look for an agent who is devoted to your real estate goals and builds strong relationships with clients that often last long after closings. The best agents enjoy serving their clients, collaborating, problem-solving, and supporting them every step of the way.

How to Financially Prepare as a First-Time Home Buyer

While there are many steps in the home-buying process, it’s best to start by reviewing your finances, especially as a first-time home buyer. In fact, you should do this long before you start looking at homes. While diving into your finances can feel daunting, our partner at Penrith Home Loans is here to help. Cherie Kesti is a Branch Manager and Mortgage Consultant who also happens to be a Kitsap County local. With more than 20 years of experience working in the home financing industry, she was happy to answer these common questions from first-time home buyers.

What are the top things lenders consider when working with a first-time home buyer?

There are a lot of things we look for when qualifying a first-time home buyer, but four key areas are:

- Job security: Having a minimum two-year history is ideal.

- Other income sources: This includes other sources such as social security, alimony, child support, disability, retirement, and pensions. For these types of income, lenders must confirm that the money will continue being received at least 36 months post-closing.

- Credit history and monthly debt load: Having a good credit score is an indicator of your overall financial health. If yours is low, it’s important to take steps to improve your credit score before applying for a loan. Also, the amount of outstanding debt directly affects how large a loan a buyer qualifies for. If you’re able to pay down your debt, that’s ideal before qualifying for a loan.

- Assets: Some loans require a minimum amount of assets in liquid accounts such as checking, savings, and money market accounts or in brokerage, retirement, and stocks. Borrowed funds are not considered an acceptable source of funds for a home loan unless those funds are secured by an asset such as a vehicle, or property.

Is buying a home still achievable in today’s market?

Many young adults think that they may never be able to buy a home. There is so much discouraging information in the media. However, they become more optimistic after learning that there are a variety of lending strategies and programs available to help first-time home buyers. This includes programs that allow a small down payment and gift funds from a family member to be used as a down payment. There is also down payment assistance available and the possibility of negotiating a seller-paid mortgage-rate buydown to lower interest rates. All these options help with affordability and make buying a home more achievable.

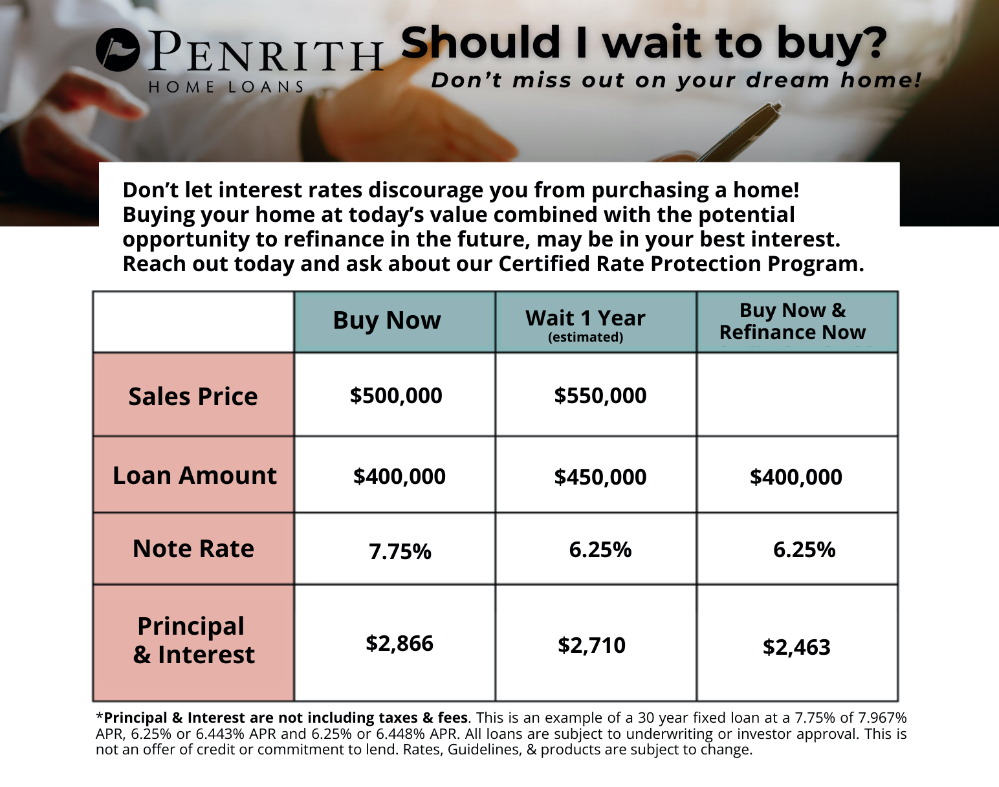

Are interest rates too high right now to buy a home?

Don’t let interest rates discourage you from purchasing a home. Buying your home at today’s value, combined with the potential opportunity to refinance in the future, may be in your best financial interest. As we say in real estate, marry the house, date the rate. If you wait to buy, most likely, the home’s value will continue to increase. This requires a larger loan regardless of the interest rate. If you buy now with a lower home value, you will have a smaller loan. With refinancing, this means a smaller monthly payment in the future.

Do I need to have a large down payment to buy a home?

If you’re saving up to buy your first home, you may be relieved to know that for most buyers, low down payment options are still available. This includes the following options:

- 0 down: The Veterans Administration and the U.S. Department of Agriculture both offer a zero-down loan program for individuals and/or properties that meet their criteria. Sometimes, loans require little or no cash out of pocket. Some down payment assistance programs also give buyers a chance to purchase with minimal down payment.

- 3.5% down: The Federal Housing Administration loan program allows as little as 3.5% down. This program is also more lenient than others on minimum credit score requirements and other factors.

- 5% down: Fannie Mae/Freddie Mac conventional loans are available with down payments as low as 3%. The minimum on these programs can change depending on factors such as property type, credit score, and occupancy. Conventional financing is now allowing as little as 5% down payment on a multi-family/2-4 family home, which will allow homeowners to occupy one unit and rent out the other units as cash flow, which offsets the expense of their monthly mortgage payment.

If you have additional questions about finances as a first-time home buyer, contact Cherie Kesti or one of our Windermere Kingston Brokers. We also have other great resources to help you, including our home-buying guide and what to examine when touring a home. Best wishes on your home-buying journey!

Should You Buy a House Now or Wait?

Many are wondering if they should buy a house now or wait. The answer is more complex than some may think. Whether you’re a first-time homebuyer, an experienced buyer, or looking for an investment property, consider the factors below.

Understand Your Market

Local real estate trends vary across the country. To better understand our local market, watch our “Market Update” video below, which includes stats for Kitsap County’s first quarter. The average home sale price is $599,000, and that’s a slight decrease of 1.2% when comparing home sale prices in 2022’s first quarter.

Windermere Kingston’s Manager, Jeanette Paulus, says, “The spring market is a great time to start looking at homes with the new listings popping up on the market.” Greater inventory could mean a shift in the real estate market.

Factor in Your Mortgage Rate

A qualified lender will be able to work with you to pre-approve you for a mortgage. Look carefully at the lender’s proposal and terms. It’s okay to get quotes from multiple different lenders before deciding on which loan to pursue.

Most homebuyers choose a 15-year or 30-year conventional mortgage. However, mortgages come in all shapes and sizes. There are first-time homebuyer programs, VA loans, and other loan programs available. Here at Windermere, we’re proud of our partnership with Penrith Loans, and Mortgage Consultant, Cherie Kesti is a great local resource. The popular real estate saying, “you marry the home but date the rate” is important to consider. Rates do change, as we’ve really seen in the last few years. So if you’re financially ready to buy and the timing is right for you personally, you can refinance down the road. As Windermere’s Chief Economist, Matthew Gardner, says, “Education is everything.” To learn more, check out his latest video on mortgage rate predictions and misconceptions.

Examine Ways to Pay Less Interest on Your Mortgage

With today’s mortgage rates, buyers are getting creative with ways to minimize their overall interest payments. Coming up with a larger down payment has its pros and cons, but it will minimize the overall interest paid on a loan.

There is also the option to do a temporary or permanent mortgage buydown. In addition, doing biweekly payments on a mortgage can significantly decrease the amount of interest paid over the life of the loan. Windermere’s home monthly payment calculator is a great tool for potential homebuyers to preview monthly payments. Crunching the numbers may help you realize whether now is or is not a good time to buy a home.

Consider Closing Fees and Other Upfront Costs

When deciding if you really want to buy a home now or wait, don’t forget to factor in all the upfront, associated costs. It is important to factor in the funds needed for insurance, down payments, and closing fees. In addition, if the sale goes through, you may have to suddenly repair or replace things like home appliances. Make sure you have a cushion if you decide to buy now. Everyone’s financial situation is different, and you don’t want eagerness or other emotions to cloud your judgment. Buying a home is often the biggest purchase that people make, so thinking about it from every angle first is crucial.

Determine Personal Cash Flow and How Long You Will Keep the Property

Knowing your personal budget and future goals will be essential for deciding if now is the right time to buy a home. For example, considering whether to buy an investment property will largely depend on your local rental market, your ability to manage the property or hire a property manager, and the property’s ability to generate passive income.

Similarly, a family who plans to stay in a home until the children are in college may be in a very different situation than a family who typically moves every two or three years for a job. Additionally, it’s important to think about how long you will have the property to avoid capital gains taxes if you plan on selling within two years.

If you’ve decided you’re ready to buy a home, check out our top home-buying tips. Windermere Kingston’s team of highly rated, local agents would be happy to guide you through the process.

Our Top Home Buying Tips

Once you start looking for a new home, suddenly everyone you know becomes an expert with advice to share. Sometimes all this guidance can be a bit overwhelming and even distracting. To help you focus on what’s most important, we’ve put together a list of our top home buying tips.

Know the Neighborhood

Many home buyers invest all their time and energy on finding the right house. The reality is you are also purchasing property in an area. While everyone knows the familiar marital phrase “you marry the family,” it’s easy to forget the same applies to purchasing a home. You marry the neighborhood. That’s why it’s crucial to do your research and make sure the neighborhood fits your needs and lifestyle.

Start by identifying a list of criteria of what is most important to you. This may include good local schools, access to parks, being close to town, a convenient commute, or a quiet community. Then make a list of things you want to avoid such as busy streets, constant construction in a developing area, or being too far from certain amenities. Vet the neighborhood by visiting the area at different times of day to gauge various activities and noise levels. Introduce yourself to the neighbors and ask them what they like about living there – it’s a great way to meet people too! Of course, we think Kitsap County is superb with top-notch schools, excellent playgrounds, awesome on-the-water activities, and fun volunteer opportunities. However, it’s all about finding the best community and neighborhood for you.

Understand All Costs and Fees

There are a lot of costs and fees associated with buying a home. Even if you’ve purchased a home before, it’s easy to forget how quickly these additional costs add up. This includes everything from estimating your monthly mortgage payment to paying property taxes. As you’re budgeting and planning, use this handy cheat sheet to make sure you include all financial obligations. The last thing you want is to be caught off guard by unexpected expenses.

Get a Home Inspection

A home inspection is key to understanding what you’re buying and also informs your budget if there are necessary repairs. Usually, a seller does a pre-listing inspection for prospective buyers to review. If for some reason this isn’t the case with a home you are interested in buying, it’s essential to have a professional home inspection done. An expert will identify potential costly repairs that are easy to miss from a walk-through such as foundation issues or roof leaks. Buying a home is a major investment, the more you know the better!

Get Pre-approved for a Loan

If you are serious about buying and want the best chance of purchasing your dream home, getting pre-approved is a must. The pre-approval process determines what size loan you qualify for. This piece of information is essential for helping you figure out what you can afford and your estimated monthly mortgage payment. Additionally, having pre-approval paperwork shows sellers your offer is financially secure and closing will be quick. It’s truly a win-win for sellers and buyers. Also, before getting pre-approved, take time to do some research and see if you qualify for any government loans. This knowledge informs the pre-approval process and ensures you receive the best loan rate available.

Work with a Local Lender

There are a variety of options available for securing a home loan, but using a local lender has important benefits. Generally, sellers and real estate agents prefer working with local lenders. Compared to online lenders and national banks, local lenders have a reputation for closing faster and on time. In addition, local lenders often have relationships within the community and possibly know your real estate agent or even the seller’s agent. All of these factors add up to a powerful combination that can work in your favor, especially if a seller receives multiple offers. If a seller is contemplating several offers, but your offer is the only one attached to a local lender, then your offer could be the one that stands out the most.

Work with a Great Buyer’s Agent

Purchasing a home is a complex transaction and something you don’t want to navigate alone. Make your life easier by working with a knowledgeable, local buyer’s agent. This expert helps find the best home to meet your needs, works with you to develop a competitive offer, prepares for negotiations, and handles all the paperwork to close the deal. Having a great buyer’s agent at your side will reduce your stress significantly. Lastly, a local buyer’s agent who really knows the area well is a great resource for you! As active community members who know the real estate market and local service providers, a local agent can connect you with other experts you’ll need such as inspectors and repair workers.

Questions? Contact one of our excellent local Windermere real estate agents.

First-Time Home Buyers: Pre-Approval, Making an Offer, Escrow

Buying your first home is a big decision. But learning more about the process will help you feel prepared and increase your confidence moving forward. Below is a list of first-time home buyers’ frequently asked questions. Read on to find out about the pre-approval process, making an offer, and escrow.

Pre-Approval Process

What is pre-approval?

Pre-approval is a way for you to establish your creditworthiness before buying a home. This is an important initial step for first-time home buyers. It helps you learn how much you can borrow. With this number, you’ll be empowered to start house hunting by knowing your price range. To receive pre-approval, you must consult with a lender to begin the process. This is a great opportunity to discuss loan options, and budgeting needs, and identify potential credit issues.

When should I start the pre-approval process?

If you have good credit and are confident in your ability to qualify for a loan, it’s best to consult with a lender when you are ready to start house hunting. Pre-approval letters are typically valid for 60 to 90 days, so it’s best to take this into consideration as you search for a home. Once the pre-approval expires, you’ll have to fill out updated paperwork as part of a new mortgage application.

If you have doubts about your credit and ability to get a loan, consider consulting with a lender approximately a year before you start house shopping. This will give you time to identify any potential credit issues and take action to address them. Also, you’ll have more time to save for a bigger down payment, which can improve your chances of qualifying for a loan.

What information is required during the pre-approval process?

The answer to this question varies slightly depending on the lender and each loan seeker’s situation. Typically, first-time home buyers need to provide an overall financial picture with proof of employment, credit information, income, assets, existing loans, and other standard identification documents. Consult this helpful pre-approval list for more information on what you’ll need to get started.

After going through the pre-approval process, Windermere Kingston Broker/Realtor, Michelle Cook recommends home buyers come in “fully underwritten.” She explains, “You will be almost as competitive as a full cash offer, which is essential in today’s fast-moving seller’s market.” Watch her full video below to learn more.

Lenders and Home Loans

How do I find a lender?

When it comes to finding a lender, it’s best to do your research. There are many options including online lenders, mortgage brokers, and local banks. At Windermere, we recommend working with a local lender to better set yourself up for success. There are several benefits of using a local lender that you just can’t find elsewhere such as a personalized experience and deep local community knowledge.

What type of home loan should I get?

Conventional loans are the most common type of loan issued to home buyers by private lenders. The two most common conventional loans are 15-year and 30-year fixed-rate mortgages. A 15-year loan means you’ll pay less interest on the loan overall. However, it requires a higher monthly payment. A 30-year loan has the advantage of a lower monthly payment, but will ultimately cost a home buyer more over a longer time period. For those who don’t qualify for conventional loans, government-backed loans might be a good option. Learn more about all the home loan options available to better understand the best option for you.

Making an Offer

How do I make an offer?

This is where having a great real estate agent is essential. Your agent will work with you to strategically craft an offer that takes into account a variety of factors including your budget and the local market to ensure it’s competitive. Also, you’ll need to have your pre-approval letter ready to ensure the seller knows your offer is backed by a lender. If your offer is under the maximum loan amount you’re approved for, it’s smart to work with your lender to get a customized letter for the offer amount. Otherwise, a seller could see the bigger number on your letter and ask for more. Lastly, make sure your down payment is ready. If everything goes smoothly, you’ll want this in place to seal the deal.

What if the seller rejects my offer?

If you’ve found the perfect home, this can be disheartening news. Sellers reject offers for a variety of reasons. It’s often part of the process. Typically, they received a higher offer. Your agent may be able to find out more from the listing agent, which can help you craft a better future offer. Regardless, don’t give up and try to learn from the experience. Your dream home is still waiting for you!

What if the seller makes a counteroffer?

A counter offer means the seller is engaged, but there are details to be ironed out. Typically, sellers request adjustments such as a higher price, a modification to your contingencies, or a change in closing dates. It’s up to you to decide whether you accept or reject the counteroffer or submit a new counteroffer. Sometimes there are multiple counteroffers until the seller and buyer reach an agreement. It’s good to discuss your price limit and flexibility on contingencies and closing dates with your agent in advance. This will help you prepare for potential counteroffers and reduce surprises.

What if the seller accepts my offer?

This is great news! While the deal isn’t yet official, you’re getting close. Once the seller formally accepts your offer, you’ll be “under contract.” This means both you and the seller have agreed to move forward with the deal. Before closing, any contingencies attached to the offer must be met by both parties. After the purchase agreement is officially signed, the purchase becomes legally binding.

Escrow

What is escrow?

Escrow is a legal arrangement where a third party holds the funds in a real estate transaction until the terms of the agreement are met. The escrow account protects the buyer’s “good faith deposit” or “earnest money.” This ensures that the deposit goes to the seller once all items in the real estate contract are met. Placing money in escrow shows the seller that you are serious about following through with the deal.

How do I begin the escrow process?

Once a seller accepts your offer, it’s time to open an escrow account. Typically, the amount deposited into the account is 3% of the purchase price or a rounded number close to that amount. After the deal is finalized and the seller has held up their side of the bargain, the funds being held in escrow will go towards your down payment and closing costs.

What is an escrow holdback?

This happens when money in an escrow account is held there after a home sale is final. Usually, this situation occurs when a buyer finds an issue with the house during a final walkthrough that wasn’t there during a previous inspection. If something unexpected happens to cause the house to be in worse condition than outlined in the contract, then the money being held in escrow is returned to the buyer, and they are released from the contract.

How does escrow work?

Once you and the seller have fulfilled all the contingencies and requirements within the contract, an escrow officer will issue you a property deed listing you as the owner. Then you’ll order a wire transfer requesting the funds to be distributed to the seller. After closing is complete, the third party managing the escrow account releases the funds. The deal is done. To learn how escrow evolves after you become a homeowner, check out this guide to escrow.

As a first-time buyer, you don’t have to navigate all these things alone. A Windermere real estate agent will help you get started, serving as your advocate and guide.